3rd Quarter 2016

“October: This is one of the particularly dangerous months to invest in stocks. Other dangerous months are July, January, September, April, November, May, March, June, December, August and February." —Mark Twain

Download Newsletter

Download Newsletter

To our clients and friends:

This quarter’s newsletter will examine the concept of behavioral finance and the importance of focusing on the long-term as opposed to being distracted by the “noise” perpetrated by the financial media. This is a theme that I’ve addressed in the past, but one which always seems to warrant further scrutiny.

Investing Based on the Calendar

Much has been written about the hazards of investing in the stock market during the month of October. The above quote by Mark Twain exposes the lunacy of thinking in terms of month-to-month fluctuations in stock prices. After all, there were very sharp declines earlier this year in the months of February, April and June.

Investing in general has become more and more dictated by emotions. These emotions are often triggered by media grandstanding. It has been shown that the biggest inflows into stocks come at market tops (“buying high”) while the biggest outflows occur at market bottoms (“selling low”). It is therefore arguable that successful “buy and hold” strategies do not reflect the typical investor’s actual experience.

The Value of Diversification

I belong to an organization called Advisors4Advisors which counts as its members a number of professional Registered Investment Advisors (RIAs) from around the country. We participate in a closed-session 60 to 90-minute webinar every Friday afternoon.

One of the favorite presenters in our group is Utah Valley University Professor Craig Israelsen who each month discusses the merits of diversification. Professor Israelsen often says “if you know the future, and know which asset class will do best in the coming year each January, then you do not have to diversify”. You would simply just put everything you have into the investment that you know is going to go up!

Wouldn’t that be easy.

However, if you conclude (correctly) that you cannot predict the future, and admit as much, then you should diversify into a variety of asset classes. As Professor Israelsen frequently reminds us, building a successful investment portfolio is akin to making salsa—the portfolio, like salsa, requires multiple ingredients in order to work.

Each of the ingredients taken by itself is of little value in the overall quest to make a delectable salsa. However, when combined with one another, these ingredients result in something much more palatable, even delicious.

Professor Israelsen extrapolates the salsa concept further into the investing realm. For the growth component of a portfolio (something he calls the “engines”) an investor is to use equity mutual funds and stocks, also known in investment circles as “risk assets” (although this does not necessarily imply that those assets have to be risky to the point of being speculative). And for downside protection—theoretically at least—he explains that the investor would use bonds and fixed income (something he calls the “brakes”).

Tweaking an Asset Allocation

This brings us to the issue of how diversification is—and is not—accomplished. After an initial asset allocation model has been constructed and implemented, an attentive investor may certainly feel it’s necessary to make adjustments to their portfolio based on the trend of the markets. But too much turnover can be counterproductive. /p>

Excessive trading in and out of the market also exposes the investor to the possibility of being whipsawed—selling lower (usually out of fear) and then buying higher at a later time when stocks have once again risen. That being said, as investors, we always hope to be on the right side of the secular (“long term”) trends in the market.

The False Allure of Market Timing

Because timing the exact stock market bottom is impossible, most successful investors opt to remain invested to a certain degree in all markets, bear or bull. This is true even if they are not always allocated to their maximum desired equity percentage

Despite a terrible decade of performance for stocks from early 2000 until mid-2009, and ignoring the recent increase in volatility, the market’s long-term trend is generally higher. Investors who wager against that primary trend do so at their own risk.

Many pure market timers will be in and out of the market at any given moment. It’s enough to make your head spin, or to induce vertigo! But trying to be completely out of stocks in order to avoid bear markets is a risky gamble. Instead, you may find yourself out of the market at exactly the wrong time. This is where “whipsaw” comes into effect.

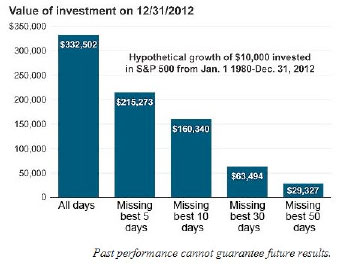

Although the following chart is a bit dated, it illustrates that over a 32-year period, if one were to miss the biggest and best days in the stock market, the growth of one’s stock portfolio would be seriously impacted, and not in a good way.

Source: Fidelity Investments

Keeping up with the Joneses

Despite the known hazards of market timing, people still do it. The greatest fear in the investment management industry is not something you might expect to hear. The greatest fear is not losing money—it is instead the misplaced fear of not making enough money when the stock market is moving relentlessly—and often inexplicably—higher.

This fear of “missing out” on gains causes great anxiety for portfolio investment managers. Many investors expectations are to match or beat “the market” in terms of performance. This is not realistic and is perhaps even delusional. Unless one is invested 100% in stocks (full risk-on), there is little hope of matching the gains of any stock index.

This fallacy in thinking can be illustrated in another example. When (or as long as) a portfolio manager is losing money when the markets are going down and everyone else is suffering the same losses, the manager will be spared from criticism. But if that manager fails to capture all of the upside gains during a spiking bull market (as in the late 1990’s), they will find themselves under enormous pressure to explain why they are lagging the indexes.

The main takeaway from this obvious disconnect in thinking is the following:

The major focus for investors, particularly those in or nearing retirement, should not be chasing the upside, but instead minimizing the downside and preserving capital.

But, in order to minimize the downside, you have to be willing to give up some upside in return. By extension this means underperforming during runaway phases of bull markets. As in the late 1990’s, recent years (specifically, 2012 and 2013) have featured runaway gains in U.S. equities. Playing defense is a necessary evil if your primary goal is to protect capital. Consequently, any defensive strategy designed to minimize downside risk over time has sometimes dramatically underperformed the stock benchmarks. In a roaring bull market, there is simply no downside to protect against. While some would view this as flaw in strategy it is the only way this type of posturing works over time.

Furthermore, there are other obstacles in implementing this discipline. Chasing upside performance results from the obsession with short-term gains and the overarching focus of some investors on making fast, easy profits from trading in and out of stocks. This mentality prevents many from taking a longer-term view. This longer-term view helps mitigate risks. And as stated earlier, excessive trading often begets greater losses.

The True Definition of Investment “Risk” is Misunderstood

Investment risk is neither 100% good nor completely evil—rather, it's a necessary part of investing. The key is to manage risk and take advantage of it in a personal way.

Warren Buffett rightfully acknowledges that people equate volatility — defined as the daily movement of stock prices up and down — with risk. But these are two different things. Buffet explains that in business schools, volatility is almost universally used as a proxy for risk. He warns "Volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray," Buffett has said.

But what is risk, really? From the perspective of the experienced, long-term investor, risk is not about fluctuations in the prices of stocks. Rather, risk is defined as a permanent loss of capital. By definition, then, runaway inflation should be considered “risk” as well. Why? Because it results in a permanent loss of capital. Is holding cash riskier than stocks? After all, you can only attempt to outrun inflation, not reverse it.

What outruns inflation? Stocks, according to Jeremy Siegel, the Wharton professor who wrote the investment classic “Stocks for the Long Run”. He has calculated that the long-term return on stocks—after inflation is factored in—results in a far more attractive "real" return than for most other investments, including cash.

Thank you for your continued interest.

Sincerely,

Andrew J.Fama, JD, AEP, RFC®, MHA, Registered Fiduciary (RF™)

Principal, Fama Fiduciary Wealth LLC

Registered Investment Advisor

*Past performance is no guarantee of future results*

*Nothing contained in this quarterly newsletter should be construed as investment advice*

![]() To download a PDF copy of this Newsletter click here

To download a PDF copy of this Newsletter click here

Disclaimer

This newsletter was produced by Fama Fiduciary Wealth LLC, an SEC-registered investment advisory services firm. The content is intended for educational and information purposes only and not as investment advice or an offer or recommendation to buy or sell an investment product. Any investment or tax decision made carries risk including the risk of financial loss and is ultimately the responsibility of the individual who should consult beforehand with a financial or tax advisor. Past performance is not indicative of future returns.

Written by Andrew J. Fama on Saturday, 15 October 2016. Posted in 2016

About the Author

Andrew J. Fama

Fama Fiduciary Wealth LLC is an SEC-Registered Investment Advisory firm originally established in 2001 under the name of Andrew J. Fama Asset Management. With over 30 years of experience representing financial institutions, businesses and individuals, Mr. Fama understands the risks inherent in all types of investments.

To learn more about Andrew J. Fama click here.

- This email address is being protected from spambots. You need JavaScript enabled to view it.