4th Quarter 2016

“Even the most intelligent investor is likely to need considerable will power to keep from following the crowd” —Benjamin Graham, from “The Intelligent Investor”

Download Newsletter

Download Newsletter

To our clients and friends:

Over the course of recent newsletters, I’ve been writing about the hazards of following the crowd when it comes to investing. The fact is that it is never a good idea to do so, regardless of how persuasive the “talking heads” on television may appear. Instead, it seems far more prudent to approach investing with a skeptical eye, and as a contrarian thinker.

It is important not to casually dismiss indicators such as investor sentiment, especially when they point to increased market risk. Of course, overriding all of this is the fact that knowledge is king. Knowledge—and information—neutralizes potentially dangerous biases (and ‘head stuck in the sand’ syndrome).

A Primary Consideration: Assessing (and Limiting) Your Risk

When assessing your risk, consider your ability, willingness and need to take the risk. A younger investor will have more ability and may have more willingness if he or she has a secure job and a regular income and is continuously adding to his or her investments. The younger investor also has more need to grow their portfolios with a larger allocation to stocks. After all, they have a longer life ahead of them.

Benchmarking (the comparing of one’s own portfolio performance and return with that of a particular stock index) subtly influences investors to be fully invested and therefore to take on more risk than they ought to in some circumstances. A flaw in the industry which is perpetuated by both investors and money managers is that one needs to keep up with the benchmark in positive markets.

For example, if the S & P 500 stock index goes up 10% and you are only one-half invested in equities (stocks), your return will likely be only about 5%. However, it is critically important to realize that you took only one-half the risk of the investor who was fully invested in the index (i.e., the market).

The expectation or desire of matching the index can be a recipe for disaster if you constantly strive for beating the benchmark by arbitrarily adding more equity exposure.

The Critical Nature of Proper Allocation

Which of these two scenarios would have a bigger impact on your life? If your investment portfolio lost 50%, or if it gained 100%? I suspect most people would answer resoundingly, “We don’t want our money cut in half.”

If the advisor listens carefully to this client, it will clarify the way the advisor approaches investing and risk—and how they actually manage money on behalf of that client. The smart advisor will focus on strategies that mitigate the loss of assets.

During both the 2001-2002 and 2007-2008 bear markets, many investors who lacked proper guidance at the time were forced to change their lifestyles—go back to work, work longer, save and invest more to “catch up” from the realized or paper losses.

For any investor in or approaching the withdrawal stage of their investing life, holding on throughout those volatile times was challenging. Those who did hold on were amply rewarded, by recouping all of their losses, and then some, in subsequent years.

To avoid bad outcomes, the investor needs reasonable expectations, clear asset selection and allocation, as well as the proper asset location (determining if an investment is placed in a tax-deferred vs. taxable account). One must also have a systematic and disciplined approach to allocating one’s money given one’s current circumstances.

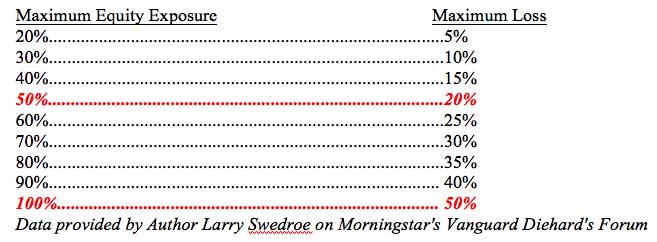

A Look at Historical Market Losses - Downside Risk

One can also get a fair perspective on risk by looking at actual stock market losses (losses which were incurred) as compared to how much money was allocated to stocks.

The table below represents estimated market losses encountered in the brutal 1973-74 bear market. A bear market is normally defined as a market decline of 20% or more in the stock indexes. Drops of 10% to 15% are called corrections. Losses of 15% to 20% are known as intermediate corrections. Anything under 10% is called “noise.”

Note in the table that a 100% stock portfolio lost nearly 50% of its value in two years. If you had 50% stocks and 50% bonds, your loss would have been limited to 20%.

Behavioral Discipline (Plus Diversification) is Key

When someone has many years to go until they need their money to actually live on—and if they have a reliable income—larger percentage investment losses might be tolerated, with the expectation of later recovery. When the retirement timeline is getting close, however, that person may want to reduce their allocation to stocks to reduce the risk of a more permanent loss.

The best way to measure investing success is not necessarily by beating—or even matching—the stock market, but by whether a financial plan has been put in place, along with a behavioral discipline that is likely to get the investor where they want to go.

If the investor can mitigate a loss of 30%, 40% or 50% in a portfolio (which is akin to negative compounding) and is not being forced to dig themselves out of a hole, it’s not necessary to beat a stock benchmark in order to do well over the long term.

Consequently, vehicles such as cash, fixed income (bonds), alternative investments and non-correlated assets (those which do not follow lockstep in the direction of the market index) have a very important role to play in an investor’s portfolio over time.

Index Investing- Do Investors Really Understand the Risks?

When speaking with other financial professionals I often hear an underlying theme. Clients wonder if they’re “doing okay” since they are not tracking the S&P 500 index or the Dow Jones Industrials. It seems that some clients are disappointed in their performance. They ask, “Shouldn’t I be invested in ‘the market’?"

Of course, no one discusses the definition of what exactly is meant by "the market". The "market" is more than just the 30 stocks in the Dow Jones Industrial Average or the 500 U.S. stocks in the S & P 500 index. Instead, the market consists of all stocks, all bonds, and all asset classes around the globe—developed and emerging.

An investor might even ask: “Why have a financial advisor at all when the Dow Jones Industrials Average keeps going up? Why bother diversifying into international stocks, fixed income, balanced funds or anything other than the U.S stock market?”

On March 9, 2009, at the absolute market bottom, no one said to buy U.S. equities (other than Warren Buffett). Now, after 7 years of strong stock market gains, everyone is enamored with the idea of passive index investing. Thoughtful and cautious financial professionals—those whose job it is to manage risk as well as return through diversification—are struggling to preach heightened vigilance with their clients.

Asset allocation and diversification certainly seems like a bad idea when you have a year like 2013 when the S & P 500 index skyrocketed. There is a pervasive tendency to chase past performance, regardless of risk or understanding that the future is not the past.

The Value of Using a Professional Advisor

Emotion can become more powerful than logic. This is especially true following a strong rise in the U.S. stock market. It seems that the fear of missing out may be starting to replace the terrible memories of the deep stock losses sustained in 2008.

For professional advisors, the opportunity to help comes in educating their investor clients about risk, behavioral finance and diversification. They can also discuss things like the negative compounding (handling losses) referenced earlier in this letter.

Financial planning and the giving of advice is primarily about managing investor behavior. It’s about the advisor helping their client make good financial decisions (and perhaps more importantly, avoiding bad ones).

This is why some industry experts suggest that financial planners consult with their own financial professional—to separate the emotion from the reality. As Abraham Lincoln famously stated about attorneys: “He who represents himself has a fool for a client.” This is why I am always open to advice and suggestions from my peers and colleagues. If you’re already retired, consulting with a financial planner can smooth out the bumps with respect to withdrawals and market fluctuations.

If you’re within 5 years of retirement, the planner will inventory your goals and work to merge them into a viable plan which will keep you on track for achieving those goals. This is really what financial planning is all about.

Conclusion

Let us never forget that no one can accurately predict the future. This applies to both short-term and long-term predictions. We should always try and remember that the path we take sometimes matters more than the destination. Risk and volatility matter.

While the stock market has historically provided far greater returns than any other investment class, the ride has often been a rough one. If an investor isn’t psychologically prepared for the ups and downs in advance, they may hurt themselves with poor decisions. This is why it may be prudent to work with a well-rounded financial planner.

Thank you for your continued interest.

Sincerely,

Andrew J.Fama, JD, AEP, RFC®, MHA, Registered Fiduciary (RF™)

Principal, Fama Fiduciary Wealth LLC

Registered Investment Advisor

*Past performance is no guarantee of future results*

*Nothing contained in this quarterly newsletter should be construed as investment advice*

![]() To download a PDF copy of this Newsletter click here

To download a PDF copy of this Newsletter click here

Disclaimer

This newsletter was produced by Fama Fiduciary Wealth LLC, an SEC-registered investment advisory services firm. The content is intended for educational and information purposes only and not as investment advice or an offer or recommendation to buy or sell an investment product. Any investment or tax decision made carries risk including the risk of financial loss and is ultimately the responsibility of the individual who should consult beforehand with a financial or tax advisor. Past performance is not indicative of future returns.

Written by Andrew J. Fama on Sunday, 29 January 2017. Posted in 2016

About the Author

Andrew J. Fama

Fama Fiduciary Wealth LLC is an SEC-Registered Investment Advisory firm originally established in 2001 under the name of Andrew J. Fama Asset Management. With over 30 years of experience representing financial institutions, businesses and individuals, Mr. Fama understands the risks inherent in all types of investments.

To learn more about Andrew J. Fama click here.

- This email address is being protected from spambots. You need JavaScript enabled to view it.